Almost a century on since the first true branded residence, and the sector has grown rapidly, particularly over the past 20 years. Flora Harley explores the latest data to understand what is behind surging demand for the sector, plus premiums commanded by the most sought-after residences.

A Century of Evolution

The first true branded residence, the Sherry-Netherland hotel in Manhattan, opened its doors in 1927. Almost a century later, there are more than 400 branded residences across the globe, the majority of which are hotel branded, according to Knight Frank Research.

Growth has been underpinned by demand for the product. More than one in three prime international buyers (39%) would be willing to pay a premium for a branded residence, according to our survey of more than 900 Knight Frank clients globally. That figure rises to 45% and 43% in Australasia and Asia respectively.

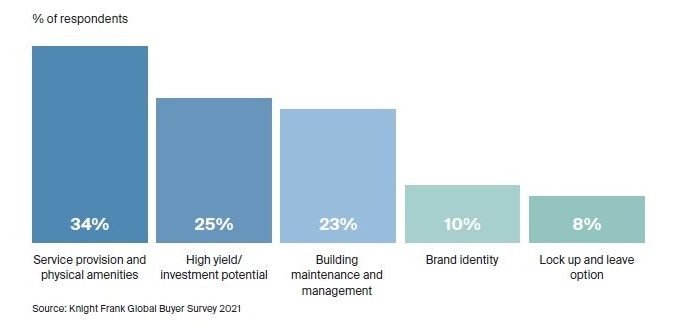

The key motivation for purchasing a branded residence is the service provision and amenities. Second comes the development’s high-yielding potential, while in third place is the building’s management and maintenance.

Q. Would you be willing to pay a premium to purchase a property in a branded residence development? (% of respondents)

39% of respondents would be willing to pay a premium for a branded residence

Q. If you were to purchase a property in a branded residence, what would be the key motive behind your purchase?

Services and amenities are the top motives behind the purchase of a branded residence

Premium Living

As outlined in the development profiles in this report, drivers of demand vary from scheme to scheme. Whilst a brand association and its benefits may result in a premium in any region, the additional value varies substantially. Defining factors and special features, such as historical legacy or park views, can also influence the price that buyers are willing to pay.

Indeed, our research shows that there is great variation on price differentials between global cities, and even within cities. Price premiums can vary from as much as 132% in some cities in Asia, to there being no differential at all. Typically, the premiums are between 25% and 35% comparable to non-branded product.

A deep understanding of micro markets is required in assessing the business case for any branded concept.

Click here for the full report.